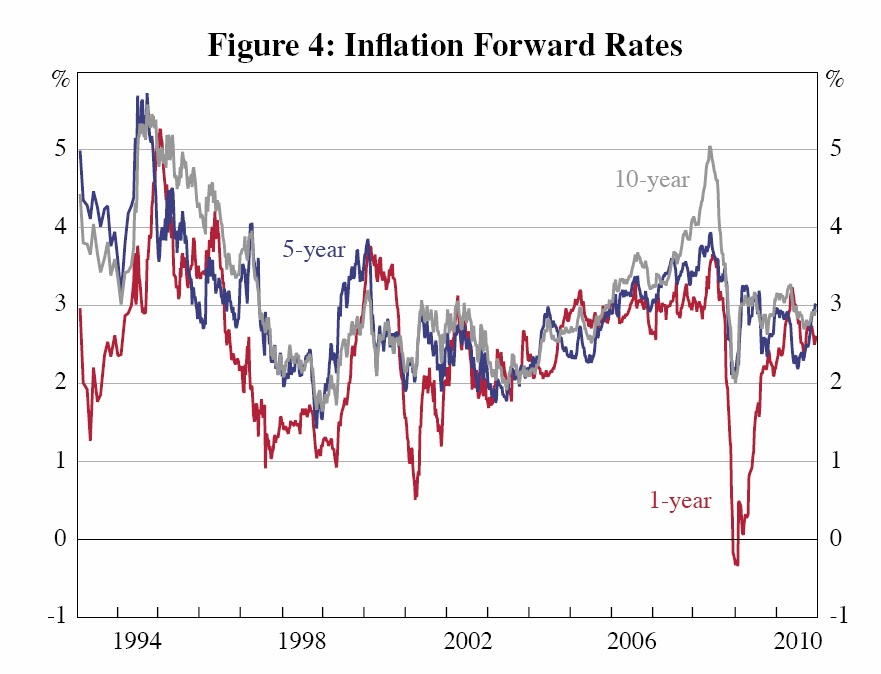

"The inflation forward rate reflects the relative prices of traded nominal and inflation-indexed bonds and is given by the sum of inflation expectations and inflation risk premia. As estimates of longer-term inflation expectations are relatively stable, movements in the 5- and 10-year inflation forward rates tend to be driven by changes in estimated risk premia. The inflation forward rate, as shown in Figure 4, generally falls during the first third of the sample, rises around the time of the GST, and rises between 2004 and 2008, before falling sharply with the onset of the financial crisis then rising again."

Of course, these are just investor inflation expectations. An equally, if not more important, benchmark is consumer expectations. The Melbourne Institute consumer survey results are enclosed below. The pink (green) line is the 60 (90) day moving average. Expectations have been heading in one direction since the early 2000s...