Now remember that this came from the same man who during the GFC told us that the price of Australian housing was going to “fall by 40 per cent or so in the next few years”, that a depression in Australia was “almost a certainty…best case scenario is a recession more severe than 1990 lasting one and a half times as long”, that Australia’s unemployment rate would rise to “double digits”, that we would have “the most severe downturn we’ve ever had”, and that his forecasting track-record was “pretty close to 100 per cent.” You get the drift. Of course, it makes for terrific media fodder.

Sadly for Dr Keen, RP Data-Rismark’s July house price index results have proven him wrong yet again. After a large 1.0 per cent seasonally-adjusted fall in the month of June, Australian home values were little changed in July, recording a raw increase of 0.1 per cent (+0.4 per cent seasonally-adjusted). The previously-reported June quarter result was revised down slightly to -0.1 per cent (was +0.1 per cent). Put more bluntly, there is no acceleration in house price losses to be seen here.

After six interest rate hikes by the RBA, the July index results afford further evidence that Australia’s housing market is experiencing a very controlled, soft-landing from the one per cent per month growth rates witnessed earlier in the year. We have been forecasting just such an outcome since late 2009.

In the period between end 2008 and March 2010, Australian home values rose by 16.3 per cent, which preserved their one-for-one relationship with disposable household incomes since 2003 (see chart). In 2010, disposable household incomes are projected to rise by around 4-5 per cent. Unsurprisingly, dwelling prices have only accreted by 4.2 per cent (seasonally-adjusted) in the year-to-date. In the second half of the year Rismark expects to see the housing market track sideways with the possibility of modest gains if rates remain in check and economic conditions continue to improve.

The deceleration in capital growth rates is evident right across the ‘cheap’, ‘middle’ and ‘expensive’ suburbs tracked by the ‘stratified’ version of RP Data-Rismark’s hedonic index. This index shows that while the most expensive 20 per cent of capital city suburbs generated the highest gains between December 2008 and March 2010, these same areas have suffered the most substantial falls in home values in the period since (see chart). A similar pattern asserted itself prior to and during the GFC.

RP Data-Rismark’s ‘rest of state’ hedonic index, which covers the 40 per cent of all homes not situated in capital cities, illustrates that regional markets have also experienced a synchronous slow-down with house values off by 0.2 per cent since April 2010. In recent times, housing costs have risen comparatively more slowly in the rest of state markets. Between end 2008 and July 2010 house values in the rest of state areas rose by 8.5 per cent compared with 16.1 per cent growth in the value of detached houses located in capital cities.

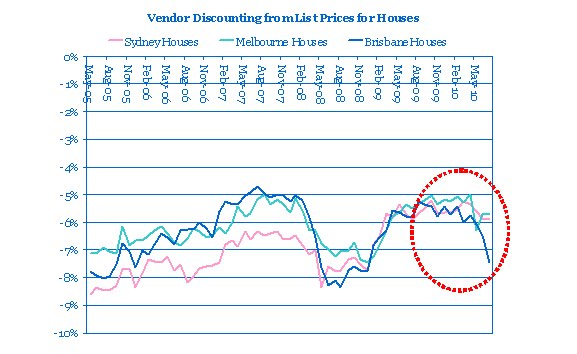

RP Data’s leading indicator data portends a relatively positive outlook. After falling from historically high 70-80 per cent levels, national auction clearance rates have recently stabilised at around the 60 per cent mark (see first chart below). While outstanding inventory levels have expanded in response to weaker demand, they have also settled (see next chart). And vendor discounting in Sydney and Melbourne is still well above 2008 levels, although we have noticed a more striking increase in the size of discounts offered in Brisbane.

Perhaps most significantly, the futures market is currently pricing in no further rate hikes over the next 1-2 years. In recognition of the flat yield curve, some banks have started cutting the cost of their fixed-rate loans, which will support demand for this otherwise unpopular product (the vast bulk of all loans are variable-rate).

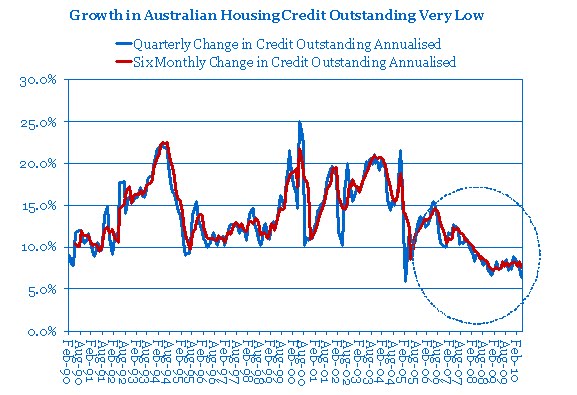

Looking forward, I would expect to see the banks pushing housing credit growth a little harder as the profitability gains—driven by reduced impairment provisions across their business lending books—dissipate. Australian housing credit growth has been running at record low levels (see next chart), and has experienced a downward trend since 2006. An increase in credit growth back to higher single digit levels could supply a boost to the market in the next 12 months.