"2007 is looking eerily similar to 1987, at least judging by the equities market performance thus far...The bad news for equities investors is that it took until almost 1997 for the market to consistently recover its post-crash peak. Here's to hoping it does not take 10 years for the ASX to breach 6,800pts. (Note the 'dead-cat-bounce' in 1994.)"

In 2011 the Aussie sharemarket is still 37% below its 2007 apogee with countless false dawns heralded by stock spruikers as the beginning of a new year of double digit returns. It is an instructive exercise to troll back through either Business Spectator or the Australian Financial Review's "annual predictions" of where the sharemarket will be in 12 months hence. It does not look pretty: according to the All Ordinaries Price Index, shares have delivered no net capital returns since 2005 (see chart).

Global shares have not been much better, and super funds, with their unnecessarily high weights to all forms of equities (another problem we have warned about for many years), have not protected investors. In fact, according to Super Ratings, the average "balanced" or "conservative balanced" super fund has underperformed inflation over the last five years--that is, they have delivered negative "real" returns. The numbers look even worse if you allocated to any of the "growth" options offered by your super fund. Before inflation, the average five year return has been 0.5% to 1.3% per annum (after inflation, returns are substantially negative).

Australian cash and fixed-income have been safe harbours during this turbulent time. Yet as the European sovereign debt crisis continues to rock the world, the risk is that the RBA temporarily "looks past" brewing inflation pressures, as many are calling on them to do, and cuts interest rates.

In this respect, US investors have the worst of all possible outcomes: high inflation; low growth; low interest rates; and an extraordinarily volatile equities market. Many smart observers are recommending investors seek out "inflation hedges" in our increasingly stagflationary world, such as gold, commodities and even bricks and mortar. After years of selling their gold reserves, central banks are back buying again. And only yesterday Bloomberg published an article with the headline "London Home Prices Surge as Investors Turn to Property Amid Market Turmoil."

The inversion of the yield curve that I have been talking about regularly here has started reducing the term deposit rates offered by Australian banks. The concomitant benefit is that the price of fixed-rate home loans has also declined. If the RBA loses its nerve and cuts its official cash rate, I think we will see more capital shifted back into housing given its demonstrated value as a (relatively) safe store of wealth. This is one of the internal inconsistencies the extreme bears face: a recession means home loan rates are going to plunge, which will only help house prices in the unique Australian market where almost all debt is variable-rate.

While the Aussie sharemarket is still nearly 40% below its 2007 peaks, Australian house prices are about 10.3% above their pre-GFC highs. Notwithstanding this, we have had effectively no house price growth in nearly one-and-a-half years while household disposable incomes have, according to the ABS, raced ahead at an 7-8% per annum rate.

As other wise-heads have observed as we bounce from one crisis to the next, bad news sells and many cannot help themselves when it comes to peddling the end of the world. The online editors at the Sydney Morning Herald are a case in point, and especially fond of promoting doom-and-gloom.

For example, last month RP Data-Rismark reported that house prices in Australia's largest city, Sydney, had risen despite national values falling. The SMH nevertheless focussed on the national findings and subordinated the Sydney results, running with the headline "Prices fall faster in July" when, in fact, Sydney prices had actually appreciated slightly.

If I search out "housing" or "house prices" on the SMH's website, recent headlines include, "Sydney housing in dire trouble", "Housing out of reach for many", "Housing shortage a myth, bears claim", "Domino effect shows as gloom spreads to housing", "House prices to stagnate as debt binges end", and "House prices to slide further in 2012".

Now contextualise these claims against the hard fact that Australian capital city dwelling prices are merely 2.9% lower than their level of 12 months ago. That is substantially less than some of the more savage daily swings in the sharemarket. Including rents, total gross returns realised by property investors have been positive!

A more balanced analysis is that while the housing market is certainly soft, it is not collapsing, and, if truth really be known, we are seeing some partial, leading indicators that imply the market may be finding a base.

The near-term outlook is, as I have been at pains to emphasise for the last 12-18 months now, heavily dependent on the course of interest rates, and, it would more recently appear, community perceptions of such.

The conviction households have held that they would be smashed with at least 2-3 rate hikes this year has exacerbated the subdued conditions. But the hikes have not materialised, and economists, the financial markets, and journalists are all talking about the prospect of cuts, or at least rates remaining on hold for an extended period.

Combined with a falling currency (currently down nearly 10% from its recent highs at just 1.018 US cents), which will help exporters and ex-pat demand for local homes, it is plausible that Australia's housing market is rapidly approaching a turning point.

The final judge of this matter will, of course, be the house price data. But today it is instructive to review some of the aforementioned leading indicators. I would highlight three in particular.

The first chart below shows the monthly number of AFG housing finance applications, which in August hit its highest level in 19 months. (AFG is Australia's largest mortgage broker and accounts for about 10% of the market.) The three month moving average is also trending up solidly following the flood-induced trough in January.

The second chart of interest illustrates the share of first time buyers as a proportion of all borrowers. According to AFG, this hit a low of 9.5% in June 2010 and has gradually increased since to 13.8% in August 2011 (the enormous protrusion in the middle of the chart depicts the stimulatory effects of the government's first time buyer boost). That is to say, there is some early evidence that first time buyers are returning to the market given the improvement in housing affordability (ie, lower house prices in concert with robust disposable income growth).

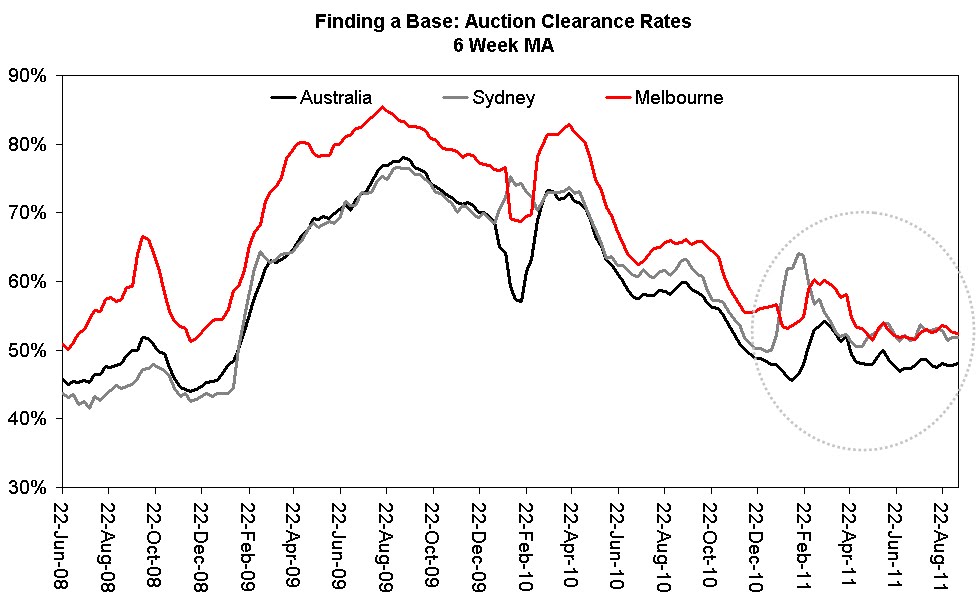

The final chart shows weekly auction clearance rates for Sydney, Melbourne and a weighted-average of all capital cities (noting that the auction sales mechanism is more common in the two biggest conurbations). What we can draw from this is that since the second quarter of 2011 clearance-rates have stabilised at slightly above 50% in Sydney and Melbourne, and slightly below this level across the combined capital cities. That is, there is no sign of a continued deterioration.

The housing market probably needs a little more time to get accustomed to the striking change in interest rate expectations (ie, from several hikes to no hikes, or even cuts, if you believe AMP, Deutsche Bank, Goldman Sachs, Westpac or Macquarie). For what it is worth, I have not altered my own views, and still expect the next move to be up. But set against the cacophony of voices calling for easier monetary policy, my own opinions are likely irrelevant for overall consumer behaviour (having said that, consumers have had similarly hawkish perspectives to this point).

The next major marker will be the August house price index data. This will be a crucial guide to whether Australia's housing market is experiencing an accelerating decline, as folks like the perennial doomsayer Steve Keen would have us believe, or treading water, as I think is much more likely.