The first is the likelihood that the June quarter inflation outcome released in a few weeks will ‘print’ on the acceptably high side. And ‘high’ is anything equal to greater than a 0.8 per cent quarterly increase in the RBA’s ‘core’ or ‘non-volatile’ measures of inflation. This would mean that underlying inflation is running at more than three per cent per annum, which breaches the upper bound of the RBA’s formal, through-the-cycle target of two to three per cent per annum.

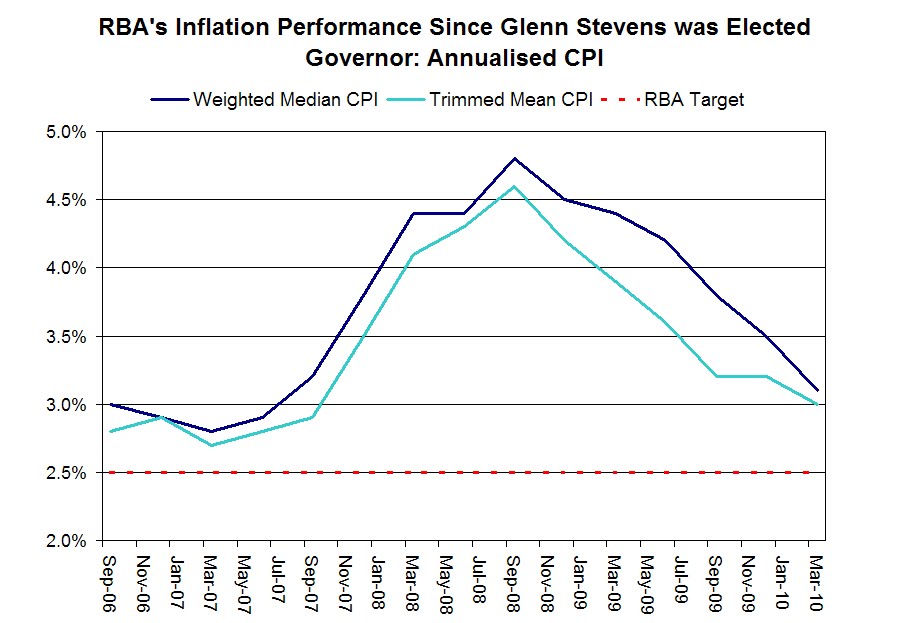

While the RBA can temporarily tolerate higher periods of inflation beyond its target, Australia has been suffering from excessive inflation for nearly three years now. Indeed, as the chart below shows, three-quarters of Glenn Stevens’ term as Governor has been characterised by core CPI above the target range. This means the Governor runs the risk of reneging on the accord he signed with Treasurer Wayne Swan in December 2007, which committed the RBA to “keeping consumer price inflation between 2 and 3 per cent, on average, over the cycle. This formulation allows for the natural short-run variation in inflation over the cycle while preserving a clearly identifiable performance benchmark over time.” It is doubtful whether anyone at the RBA seriously considers three years or more as ‘short-run’.

We are supposed to be coming out of a period of weak economic growth during which time the RBA would have ideally liked to see inflation fall to a cyclical trough of two per cent or less (thereby also dragging down the through-the-cycle average). The fact that the nadir in Australia’s current inflationary cycle has been stuck belligerently above the RBA’s acceptable target raises grave credibility concerns for the central bank. And there are few things more important to a central bank than its credibility.

The main determinant of future inflation is our expectations of it (this is similar to George Soros’s ‘reflexivity’ principle). The more punters get used to living with annual price rises of greater than three per cent, the harder it will be to wrench those expectations back into the RBA’s preferred range. (Boffins will also note that the RBA’s target of two to three per cent is already on the sympathetic side of the acceptable range embraced by other central banks.)

A related point that would be giving Martin Place pause is that Australia’s experience with low and stable inflation is only a recent innovation. The last two decades of benign price rises have enabled the RBA to keep nominal interest rates at half the levels experienced in the decades prior to the 1991 recession. Older heads know that it took searing mortgage rates of 17 per cent and a recession that saw unemployment peak at around 11 per cent for the RBA to crush the inflationary demon. The Bank will want to do everything possible to avoid having to administer this extreme medicine again.

The second driver of any near-term rate hike is the mixed blessing that is Australia’s stunningly low unemployment rate. Just as inflation has remained stubbornly high, joblessness probably did not increase as much as the RBA might have liked when thinking purely about price stability.

After hitting an all-time low of 4.0 per cent in March 2008 (at least since quarterly ABS records began in 1978), Australia’s unemployment rate peaked at only 5.8 per cent in October 2009, which, as Alan Kohler has observed, was the exact reverse of the 8.5 per cent outcome many expected during the GFC. The problem with this is that according to official forecasts Australia’s economy is about to embark on at least two years of above-trend economic growth with little-to-no spare skilled labour capacity to accommodate this expansion.

But the news gets worse for our first female prime minister, Julia Gillard. A fascinating new report released by the RBA last week, which for some reason has been overlooked by the mainstream media, finds that the two variables discussed above—inflation and unemployment—are tied to one another via a troublesome trade-off over at least the medium term.

In short, you cannot reduce unemployment beyond a certain threshold without invoking inflationary pressures. What makes Australia’s present circumstances especially challenging is that at the inception of a new terms of trade boom the jobless rate is already smack-bang in the middle of the 4.75 to 5.25 per cent range that most believe is the level beyond which further labour demand risks inducing wage-price spirals. These dynamics have been arguably exacerbated by the recent empowerment of Australia's labour force to make wage claims under the more worker-friendly policies of the current government. Here it pays to recall that one of the chief reasons why the so-called ‘non-accelerating inflation rate of unemployment’ fell from seven to eight per cent in the 1990s to around five per cent today is because of the liberating labour market reforms first implemented under the Hawke and Keating governments.

The bottom line is that the RBA is unlikely to allow unemployment to fall much further. In last week’s RBA report, two economists, David Norman and Tony Richards, declared that the age-old ‘Phillips curve‘—which posits a trade-off between inflation and unemployment—is well and truly back in vogue. In particular, their analysis shows that the negative relationship between inflation and unemployment outlined under the Phillips curve model, which had been discredited by many modern economists, provides the best predictions of changes in Australian inflation over time. Norman and Richards’ research also illustrates that the standard Phillips curve model of inflation outperforms more sophisticated approaches.

Interestingly, the RBA’s standard Phillips curve model does not assume that there is no long-run trade-off between inflation and unemployment. This latter thesis was fashionable in the modern economics literature, which purported that participants were able to accurately anticipate, and thus negate, monetary policy in the long-term. Indeed, when the RBA tries to incorporate this adaptive expectations assumption into its models, their performance deteriorates.

So is there anything that we can do to cut this Gordian knot? As with most things, the answer lies in ourselves.

Australia is in the enviable position of being a high-growth economy with an extraordinary endowment of natural resources that can be profitably exploited care of the urbanisation and industrialisation of the world’s two most populace nations, China and India. We are able to leverage off this seismic shift in the structure of the global economy at a time when most of our peers are predicted to endure protracted periods of sub-trend growth.

But Australia also faces a major obstacle if it is to capitalise on the swing in global economic output away from the eurozone and anglosphere towards the Middle Kingdom: shortages of people. And this paucity of skilled labour will be made worse as our nation ages, with the working share of Australia’s residents forecast by Treasury to decline strikingly over time. As the number of income producers in the community falls, and the ageing of the nation imposes greater health and medical demands on us all, the tax burden on those remaining workers will rise. One tangible manifesation of this problem is Treasury's forecast that Australia will run perpetual fiscal deficits between 2030 and 2050.

As I have argued here, like any other high-growth company, Australia is ‘short’ human capital. This reconciles why an ostensibly xenophobic Coalition government oversaw one of the biggest increases in skilled migration in Australia’s history, and why our population growth rate has recently ranked among the highest in the developed world. The Treasury also acknowledges that higher immigration would ameliorate the adverse effects of an ageing population by generating stronger growth and a deeper revenue base.

While there are well-known challenges to absorbing a substantial increase in the number of permanent residents over time, there is no reason why these cannot be met with sensible energy, infrastructure, and urban planning strategies, which, crucially, have to be coordinated and funded by Federal and State Governments working as one.

By proudly slashing our foreign labour intake in the name of scoring below-the-belt political points, the Federal Government is directly contributing to capacity constraints and inflationary pressures. And they will be ultimately culpable for forcing higher interest rates if they do not seek to manage Australia’s prosperity with more prudent polices.

What we need to do is change the tenor of our political rhetoric. Lower immigration might mean a little less congestion in the short-term. But it will also translate into higher inflation and higher interest rates. Lower immigration and slower population growth will also exacerbate the economic problems spawned by the ageing of our nation. In particular, cutting back on our investments in people today will result in higher taxes for all future generations of workers.

Both sides of politics need to be more mature, responsible and forward-thinking in their public approaches to confronting what is arguably equivalent to a major national security concern (indeed, The Australian's commentators have claimed that a larger population is a national security imperative). Here the Coalition has much to answer for by pushing myopic and populist outcomes, which has compelled the government into lowest-common-denominator responses.

The next time residents in South West Sydney complain about immigration (ignoring the fact that more than one-third of them were born overseas), why can’t the Gillard Government commit to investing in more public transport, roads, hospitals and schools rather than thumping boat people or advocating a smaller Australia? Why not provide policy solutions that allow us to absorb and liberate growth as opposed to restricting it?

The simple fact is that with little government debt Australia can afford to make the major investments in high-value public amenities required to get the community across the line on the ‘Big Australia’ vision. And given the vast tracts of habitable land situated along most of our island continent‘s coastline, there is no reason why we could not, in principle, support a population base multiples its current size with appropriate investments in energy, transport and urban planning technology.

We certainly should not peg ourselves to a population level in 40 years’ time based on existing capacity constraints. Our chief aspiration must be to commit to using our ingenuity to unlock current and future bottlenecks.

As I have suggested before, the alternative is, quite frankly, Japan. A nation that has shunned immigration and is forecast to see its population shrink by up to 25 per cent over the next 40 years. A nation that has experienced two ‘lost decades’ primarily attributable to a relentlessly declining population growth rate. A nation that is being increasingly threatened with social and economic irrelevance.

The good news is that our fate is in our own hands.